At no point does the company make clear that it is going to be extracting a tenner each month from the customer's credit card or debit card.

This is not stated in the emails it sends out - not even the very first one.

Instead, it relies on two facts:

Fact 1/ That the vast majority of people do NOT read the well-concealed small print - small print that you only see if you click through to it.

This info should be on the same page as you visit to sign up, not hidden in another link, and should also be in each and every email (not hidden in a link).

At very least, the intention to extract each and every month should be made clear in the first email

Fact 2/ That a large number of people do not regularly do an itemised check of their credit card or bank statements.

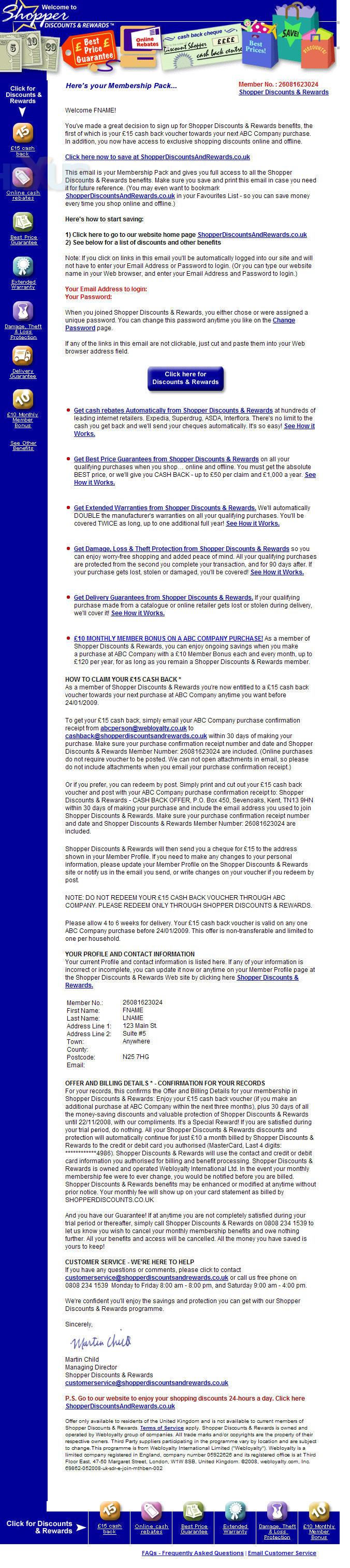

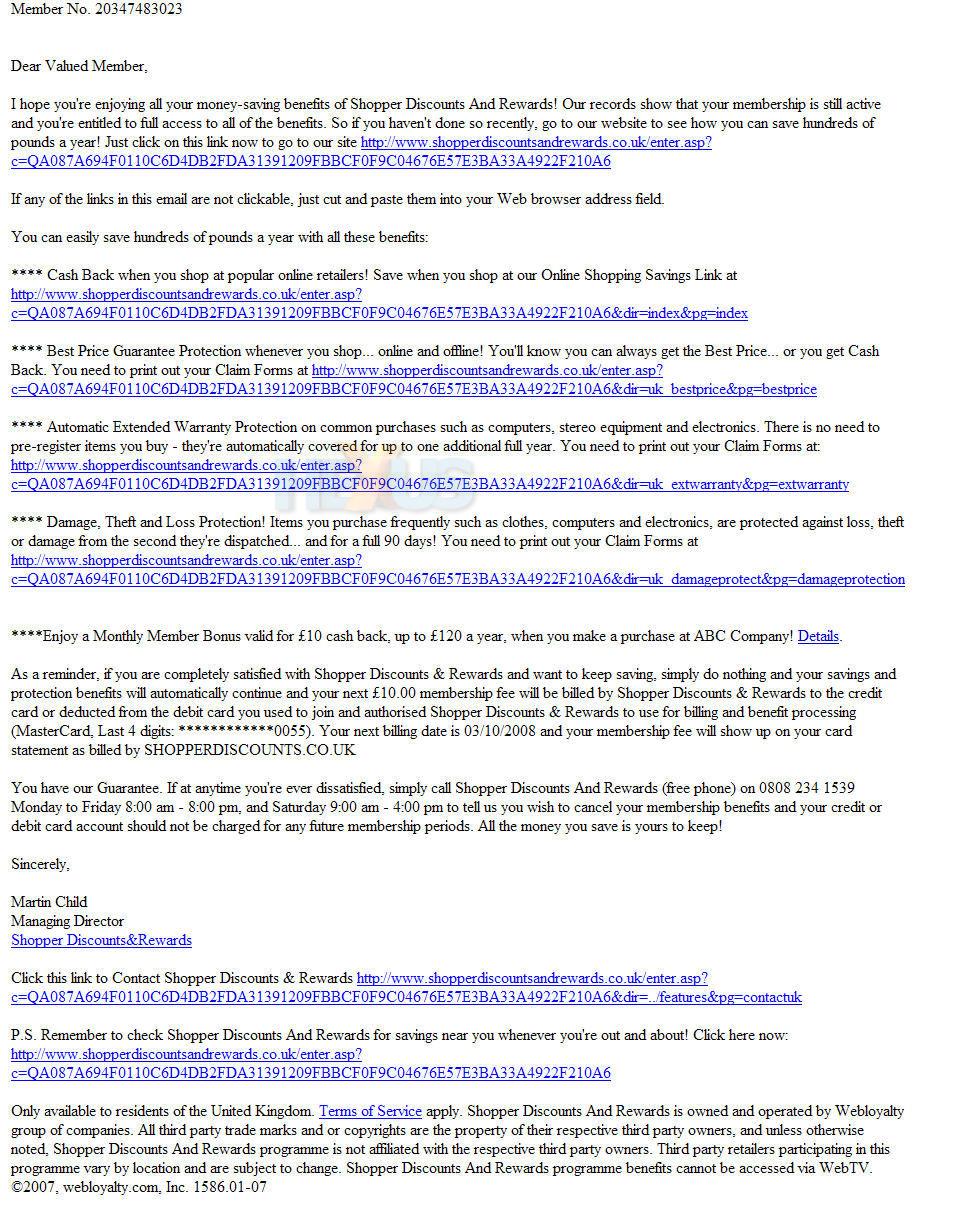

People need to look at the images that feature on the last page of Scott's latest article.

Do you see anything there about the company's intention to extract money once a month?

No, you don't - could it be because they are trying their hardest to keep this fact as well hidden as possible?…

And that's the real bottom line - they do NOT at any point make it as clear as possible, or anywhere near as clear as people think they should, that this is what they are going to do (i.e. extract money every month) - they seemingly rely on the fact that people won't realise.

EVERY organisation I've ever dealt with online that plans to extract money each month sends me an email a good few days ahead of time that the extraction is going to take place, telling me that this is what it's going to do.

This is NOT something that this outfit does and it's a reasonable presumption that this is because it doesn't want people to know.

Do the maths here - let's say that EVERYBODY catches on to what's going on sooner or later and does get their money refunded in full (two huge assumptions that are most unlikely).

And let's say that the average time it takes people to catch on is, what, three months (could be less, could be a LOT more)?

But, let's say, just for now, that it's three months.

I don't know how long these people take to refund but I'm pretty sure that they won't be

rushing to do this but let's be conservative and say the refund takes, on average two weeks (roughly half of a month).

So that means that:

After the first month, they've had a tenner of the customer's money sitting in the company's bank account for one month.

After the second month, they've had a tenner that's been there two months and another tenner that's been there one month.

After the third month, they've had a tenner that's been there for three months, another that's been there two months and yet another that's been there one month.

When it's discovered what's going on, the complaint made and the promise to refund issued, our assumed average is that the money will be in the company's bank for another half a month.

This means that one tenner has been there three-and-a-half months; another has been there two-and-a-half months; and another has been there a month-and-a-half.

So, in total, it's like having one tenner in the company's bank for seven-and-a-half months (3.5 + 2.5 + 1.5 months) - though that ignores the compound-interest-effect that means the figure is actually higher.

Now, let's guess at how many people are trapped by this in a year.

Is it only five thousand (highly unlikely me thinks)?

Let's just say it is - for now.

That could mean that this company has the equivalent of £50,000 (5,000 x £10) in its bank account for the equivalent of seven-and-a-half months (and i reckon, it will be a high-interest account of some sort).

That's actually quite a lot of interest but not mega-bucks.

Now let's look at some other possible figures for the number of people who could be unwittingly trapped.

Let's say that it's not 5,000 but 50,000 - that would be equivalent to the company having £500,000 (yes, half a million) of someone else's money that's raking in the interest for them for seven-and-a-half months.

But what if the real number of people caught in this is 100,000? And I think it's quite possible that it's more - maybe a lot more.

Well that would be like the company having a million pounds (£1,000,000) of other people's money earning high interest for seven-and-a-half months.

I haven't a clue what sort of high interest this company has been raking in - but I'd be deeply shocked if it were less than seven per cent (and, until recently, it could have been a good bit more, if they know how and where to place the money - and I bet that they do).

I'll let someone else do that final bit of maths but it's quite obvious to me that this company's choice to be less than as clear as they could be, is bringing in a huge amount of money into the company's coffers in interest alone - a percentage of which the company might not entitled to, certainly morally at any rate.

And all the above assumes that all the people who feel they've been scammed do catch on and do get all their money back.

But that strikes me as highly unlikely, so the amount of money that the company actually could get to keep is going to be considerably more than my all-refunded calculations assume.

I'll end here by re-iterating what I said at the end of my initial posting to

the first forum thread about this matter,

Someone needs to stop this sort of stuff cos it seems this mob is far from being alone - it's only one of a number who are running such a businesses which, quite understandably really, leave people feeling scammed - and until the government and other authorities take some action, such firms are going to keep on lifting money - huge sums of money in total - out of the accounts of people who've no idea at all that this is a happening until after the event, leaving them feeling ‘had’.

Bob C

28

The Facebook company's new name is Meta

28

The Facebook company's new name is Meta

14

Openreach adds 170 towns and villages to FTTP rollout plan

14

Openreach adds 170 towns and villages to FTTP rollout plan

26

Major UK ISPs ordered to block five pirate streaming sites

26

Major UK ISPs ordered to block five pirate streaming sites

{kind=link}

{kind=link}